Posted by Tim Evans in Rooflines, The Shelterforce blog, June 13, 2017 edition. This excerpt copied with permission of the National Housing Institute

While recent news reports have highlighted the low number of affordable housing projects using federal tax credits that are built in high-opportunity areas, a recent examination by New Jersey Future has found that strategic changes in the way federal funds are allocated for affordable housing in the state have meant that many more affordable housing projects have been directed away from high-poverty neighborhoods and toward areas that offer greater economic opportunity.

To evaluate whether those changes had their intended effect, New Jersey Future compared affordable housing projects that received federal Low Income Housing Tax Credits between 2005 and 2012 with projects that received credits between 2013 and 2015, after the New Jersey Housing and Mortgage Finance Agency (NJHMFA), which administers the tax credits in the state, made significant changes to the criteria it uses to award them. The agency made the changes with the specific goal of steering new construction of affordable housing away from areas of concentrated poverty and toward areas where public transit and major job centers existed, and that have higher-performing school districts.

Before the adjustment, a full two-thirds of projects near transit were located in . . .

” … we applaud efforts in Montpelier and are excited to work with local municipalities that want to make bold investments in affordable housing, realizing that such investments are winners in accomplishing Governor Scott’s three priorities: supporting our economy, making Vermont more affordable for Vermonters, and protecting our most vulnerable community members. Several proposals have been made – we welcome all efforts that satisfy each of these three objectives.”

by Michael Monte

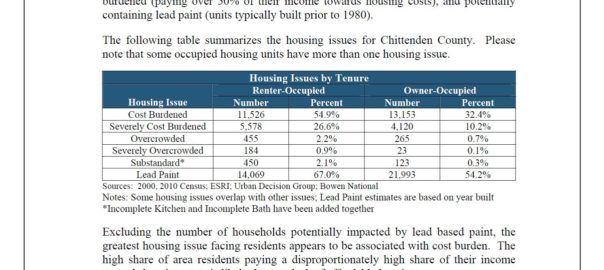

There seems to be a burst of housing construction in Chittenden County, and some are even suggesting that the tide has turned in making the rental market more affordable, or that the vacancy rate is high enough, or we’re building too fast. At the Champlain Housing Trust, our assessment is that although the trend line is improving, more needs to be done – especially for low wage earners priced out of the market, and certainly for the 350 people on any given night in the county who have no home at all.

According to Mark Brooks, co-author of a report that provides a comprehensive semi-annual analysis of the real estate market, the long-term market vacancy rate in Chittenden County is 2%. The December, 2016 report indicated a market vacancy of 4.4% – a number offered as a point-in-time rate of what’s available without taking in consideration the timing of apartments just completing construction or other factors.

This lower rate is a more accurate assessment, as it takes into account the time in which newly-constructed apartments are absorbed into the market. Most will agree that a 5% rate will yield a healthy market for renters and owners alike. While we were close at a point in time in December, we’ve not sustainably reached this target.

In the last two years alone, over 1,200 apartments have been constructed. The new construction does give some renters more choices: according to the report, “…landlords are offering incentives such as one month free rent, flexible lease terms, or lower rents.” Rent rates across the board have been stable and closer in-line with inflation – unlike the previous six years.

New households are forming every day in Chittenden County, and large numbers of people are still commuting long distances from less expensive housing in more rural counties to get to work. In fact, in 2002, 73% of Chittenden County workers lived in the county; that percentage dropped to 63% in 2014. Lack of housing opportunity is leading more and more workers to commute longer distances.

Demand is still high as younger people, sometimes saddled with high college debt, are renting instead of purchasing a new home. And employers are still viewing rents and housing availability as being barriers to economic growth. A representative of one business told us recently that her company added jobs in the mid-west instead of Burlington because of the lack of housing.

In order to push the underlying market rate from 2% to a sustained 5%, we need to continue to provide additional growth. Can we sustain this growth and increase the vacancy rate in the future? We hope so. But next year fewer apartments are on track to be coming on line, less than half the number built this year. And although there are an additional 2,400 apartments in the development pipeline county-wide, those won’t be here next year, or even the year after that.

Charlie Baker, executive director of the Chittenden County Regional Planning Commission, part of a coalition launched in 2016 that will try to bring about the construction of 3,500 housing units in Chittenden county over the next five years. Peter Hirschfield / VPR

As importantly, the resources available for affordable housing are seriously limited. Although there is enormous opportunity and capacity to build more affordable housing, the equity or cash needed to insure that rents remain affordable are not available. Non-profit owners continue to struggle with meeting the demand for more affordable housing, as evidenced by long waiting lists for subsidized housing or the 150 applications CHT gets every month for the 20-25 apartments available.

That’s why we applaud efforts in Montpelier and are excited to work with local municipalities that want to make bold investments in affordable housing, realizing that such investments are winners in accomplishing Governor Scott’s three priorities: supporting our economy, making Vermont more affordable for Vermonters, and protecting our most vulnerable community members. Several proposals have been made – we welcome all efforts that satisfy each of these three objectives.

————————————————————————————————————————-

Michael Monte, is Chief Operations & Financial Officer at The Champlain Housing Trust, founded in 1984, it is the largest community land trust in the country. Throughout Chittenden, Franklin and Grand Isle counties, CHT manages 2,200 apartments, stewards 565 owner-occupied homes in its signature shared-equity program, offers homebuyer education and financial fitness counseling, provides services to five housing cooperatives, and offers affordable energy efficiency and rehab loans. In 2008, CHT won the prestigious United Nations World Habitat Award, recognizing its innovative, sustainable programs.

“There has been a renewed interest in the role that the real estate market can play in solving our growing affordable housing crisis. For decades “affordable housing” has been the near exclusive domain of the public sector, but the crisis has reached the point where we are now calling for all hands on deck. Can private capital, private development companies, and market-rate housing developments help make housing affordable for everyone?”

…

“Housing advocates tend to agree that we need to supplement market-rate luxury development with subsidized affordable housing, but rarely do we ask the market to provide housing for people further down the income ladder. This dichotomy of new market-rate housing only for the rich and new affordable housing only for the poor has become the de facto housing strategy in most American cities. We can do better.”

– San Francisco Chronicle http://www.sfchronicle.com/opinion/openforum/article/Reform-land-use-promote-shared-growth-of-new-9283703.php

By Jason Furman | September 25, 2016 | Updated: September 25, 2016 8:34pm

Photo: Michael Macor, The Chronicle

When certain government policies — like minimum lot sizes, off-street parking requirements, height limits, prohibitions on multifamily housing, or unnecessarily lengthy permitting processes — restrict the supply of housing, fewer units are available and the price rises.

It is no secret that cities like San Francisco, New York and Washington, D.C., face challenges in the availability and cost of housing. But policymakers and economists have increasingly recognized both the role that certain inappropriate land use restrictions play in raising housing costs — not just in major cities but across the country — and the opportunity for modernizing these regulations to promote shared growth.

Basic economic theory predicts that when the supply of a good is constrained, its price rises and the quantity available falls. In this respect, the market for housing is no different: When certain government policies — like minimum lot sizes, off-street parking requirements, height limits, prohibitions on multifamily housing, or unnecessarily lengthy permitting processes — restrict the supply of housing, fewer units are available and the price rises. On the other hand, more efficient policies can promote availability and affordability of housing, regional economic development, transportation options and socioeconomic diversity.

Research suggests that local barriers have become more restrictive in recent decades. One way to measure this is comparing the sale price of houses with construction costs. This gap typically reflects the cost of buying land — which increases with tighter land use restrictions. Indeed, the gap has increased in the past two decades: House prices from 2010 to 2013 were 56 percent higher than construction costs, a 23 percentage-point crease over the average gap during the 1990s.

Of course, many land use regulations can have benefits for communities. Environmental reasons in some localities may make it appropriate to limit high-density or multiuse development. Similarly, health and safety concerns — such as an area’s air traffic patterns, viability of its water supply, or its geologic stability — may merit height and lot size restrictions.

But in other cases, barriers to housing development can allow a small number of individuals to enjoy the benefits of living in a community while excluding many others, limiting diversity and economic mobility.

This upward pressure on house prices may also undermine the market forces that typically determine patterns of housing construction, leading to mismatches between household needs and available housing.

Improving land use policies can also create benefits for the U.S. economy as a whole. High- productivity cities offer higher-income jobs than low-productivity cities and often attract workers who move from other cities, naturally bringing more resources to productive areas of the country. But when unnecessary barriers restrict the supply of housing and costs increase, then workers — particularly lower-income workers who would benefit the most — are less able to move.

All told, this means slower economic growth: Some researchers have estimated that GDP could have been almost 10 percent higher in 2009 if workers and capital freely moved so that the distribution of wages across cities was the same as in 1964.

On the other hand, smarter land use and housing policy can promote both growth and equity. While most land use policies are appropriately made at the state and local level, the federal government can also play a role in encouraging smart land use regulations. Today, the Obama administration is releasing a new toolkit at http://bit.ly/2d4dVAc that highlights best practices that localities have employed — including streamlining permitting processes, eliminating off-street parking requirements, reducing minimum lot sizes, and enacting high-density and multifamily zoning policies — to reduce overly burdensome land use restrictions and promote mobility and economic growth.

Reforming land use policies can have important benefits for local residents and the nation as a whole, not only raising economic growth, but ensuring that its benefits are widely shared among all Americans.

Okay dear readers, this is a wonky article but for those of you interested in HUD’s Affirmatively Furthering Fair Housing rule it is a good read. (Ted Wimpey)

“For most of the Fair Housing Act’s history, its requirement to “Affirmatively Further Fair Housing” has been largely dormant. With the advent of the new AFFH rules in July 2015, however, there is some promise that this provision might be taken more seriously.”

South Burlington, VT – Dozens of Chittenden County leaders in the fields of housing, business, local and state government, and social services announced this morning a new campaign to increase the production of housing and setting a target of 3,500 new homes created in the next five years.

“Working together we will accomplish this goal,” said Brenda Torpy, CEO of Champlain Housing Trust. “For the sake of our communities, our workers and local economy, we will educate and advocate together for more housing.”

“The housing shortage in Chittenden County has been well noted with unhealthy vacancy rates and high rents,” added Charlie Baker, Executive Director of the Chittenden County Regional Planning Commission. “Employers can’t find workers, and workers themselves spend more time in commutes and with a higher percentage of their paychecks on housing costs.”

Twenty percent of the 3,500 goal are targeted to be developed by nonprofit housing organizations. The remainder by private developers.

“This step-up in production will not just provide new homes and infrastructure for communities, it’ll be a boost to the economy and contribute to the tax base. Building homes together is a big win for all of us in Chittenden County,” said Nancy Owens, President of Housing Vermont.

The campaign will provide up-to-date data to the community on the need for and benefits of new housing, build cross-sector and public support for housing development, increasing access to capital, and supporting municipalities.

Beryl Satter knew something like this was bound to happen. Or, rather, to happen again.

The Rutgers historian wrote the book on an obscure form of predatory lending from the mid-20th century that victimized black home buyers when banks would not lend them mortgages. Her book, “Family Properties,” came out in 2009, on the heels of the housing crash. And as she traveled the country talking about it — about families defrauded from the homes they thought they owned, about sellers who promised home ownership but collected deposits and evictions instead — people kept approaching her.

“Pretty much everywhere I go, people say ‘I’ve been hearing about this,'” Satter says. “Contract” lending is making a comeback.

In this model, buyers shut out from conventional lending are offered an alternative: They can make monthly payments on a home directly to the seller, instead of a bank, with the promise of receiving the deed only once the property is entirely paid off, 20 or 30 years down the road. In the meantime, they have few of the legal protections of a typical home buyer but all of the responsibilities of one. They don’t build equity with time. They can be easily evicted. And if that happens, they lose all of their investment.

According to the Detroit Free Press, more homes were bought in Detroit last year using such “land contracts” or “contracts for deeds” than conventional mortgages. In a series of recent stories, the New York Times has reported that Wall Street is now betting on this market, with investors buying foreclosed homes by the thousands and selling them on contract. Earlier this week, the Times reported that the Consumer Financial Protection Bureau is now investigating the practice’s resurgence, although it is not by definition illegal.

What is particularly alarming about the trend, though, is that we’ve seen it before. In its earlier incarnation, it was an explicitly racist form of exploitation. And now it is victimizing the same groups again: mostly lower income and minority home buyers who can’t access traditional credit.

“There’s nothing new here in the slightest,” Satter says. “This is just a continuation of the same old game. That’s what’s so disturbing.”

In the earlier era when this was common, between the 1930s and 1960s, contract lending was in some cities the primary means middle-class blacks had to buy homes. Real estate agents and speculators jacked up the price of properties two- or threefold. Then when families fell behind on a month’s payment or on repairs, they were swiftly evicted. The sellers kept their deposits and found the next family.

Satter’s father, Chicago lawyer Mark Satter, helped organize black Chicagoans to fight the practice in the 1950s. He estimated then that about 85 percent of homes bought by black in Chicago were bought on contract. “It was the way you bought,” Beryl Satter says. “There was no other way.”Many of those families then struggled to keep their homes in a system that was not sustainable by design.

Atlanticwriter Ta-Nehisi Coates based his blockbuster 2014 article “The Case for Reparations”around the story of Chicago blacks who suffered under this system, the outgrowth, as he put it, of a segregated city with “two housing markets — one legitimate and backed by the government, the other lawless and patrolled by predators.”

The Times reports of what’s happening today sound eerily similar. Writers Matthew Goldstein and Alexandra Stevenson report that an estimated 3 million people have bought homes through contracts, although the numbers are hard to track given that the deals are regulated differently in each state and are not subject to the same disclosures as mortgages.

The practice is particularly common, they report, in distressed Midwestern communities like Akron and Detroit, where the government offered hundreds of foreclosed properties to investors in bulk sales. Those same investors, the Times reports, have turned around and sold the properties on contract to moderate-income buyers for sometimes four times as much.

Why now?

But why, though, would a financial scheme created in an era of sanctioned racial discrimination be making a resurgence today? Since Satter’s father tried to sue over the tactic a half-century ago, the Fair Housing Act and Home Mortgage Disclosure Act were passed. And the end of legal discrimination opened up legitimate lending to more blacks who were no longer forced into the housing market’s rapacious underworld.

But a crucial similarity between the two eras exists: Many people still can’t get loans today.

Now, this is the case because lenders have tightened their credit standards since the crash, overcorrecting for the bubble’s exuberance with historic stinginess. The Urban Institute has counted more than 5 million loans currently “missing” from the housing market — mortgages that would have been made between 2009 and 2014 if lenders used the kind of credit standards that were common back in 2001, a benchmark for more reasonable lending prior to the housing bubble.

Millions of Americans over this same time have had their credit ruined by foreclosures — in many cases because of predatory subprime lending that has now put them in the crosshairs of predatory land contracts. Minorities who were disproportionately targeted for the former are not surprisingly concentrated among those caught up in the latter.

“When the banks close down, people still need to buy,” Satter says. And so they find a way. Just as creative investors find a way to meet their demand. Land contracts are to housing whatpayday loans are to banking and Rent-A-Centers are to furniture. What people in need can’t access through credit someone is always willing to provide — for a price.

A lawyer for Harbour Portfolio Advisors in Dallas, one of the larger players in the new wave of contract lending, told the Times that the firm’s business model is “to purchase unproductive residential properties and sell them to other people who will make them productive again.” But Satter frames this differently.

“Choices that black Americans have had for housing loans have been predatory loans, or no loans,” she says. And when banks choose not to loan, she adds, this is who they choose not to loan to.“The result,” Satter says, “is a complete revival of redlining in a slightly different guise.”

This is why she wasn’t surprised to see the practice she’d studied as a historian (and lived through with her family in the 1950s) re-emerge as front-page news.

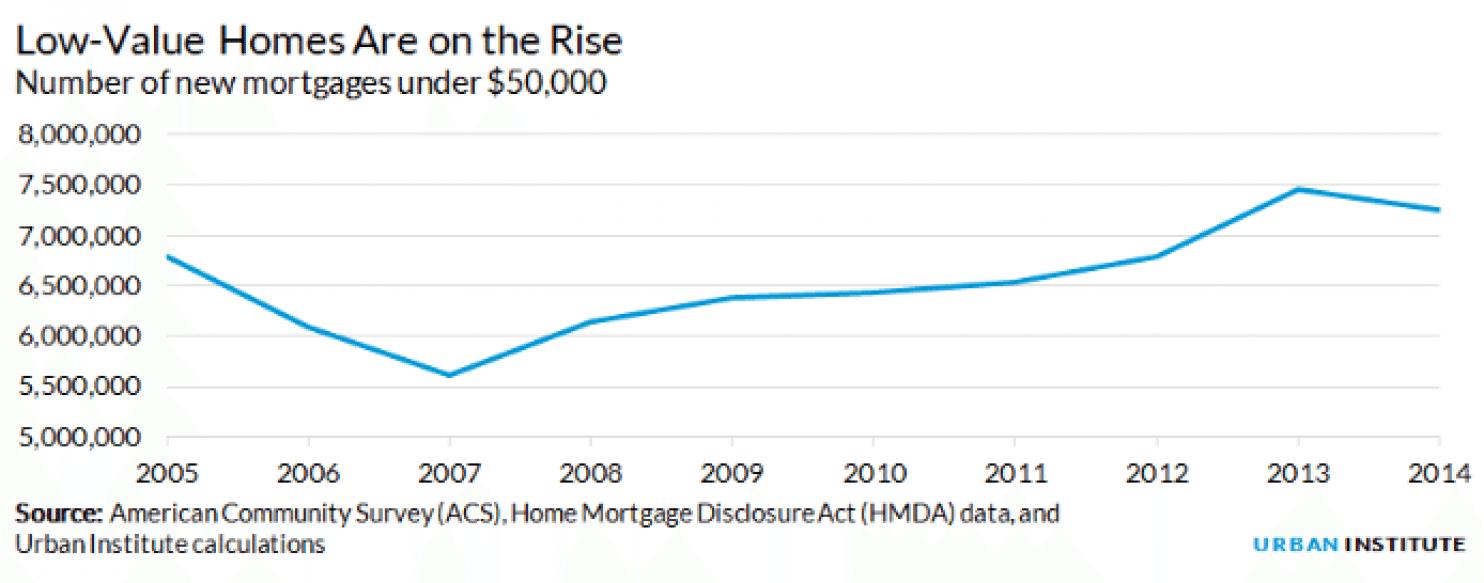

One other factor, though, helps explain why contract selling is back again. The demand among buyers who can’t get mortgages is deep. But so is the supply of houses that might accommodate buyers at the moderate end of the market. The foreclosure crisis created a vast stock of vacant homes, many of which have deteriorated through neglect. Steven Brown, an affiliated scholar at the Urban Institute, has shown that the number of homes worth less than $50,000 has been growing:

Urban Institute

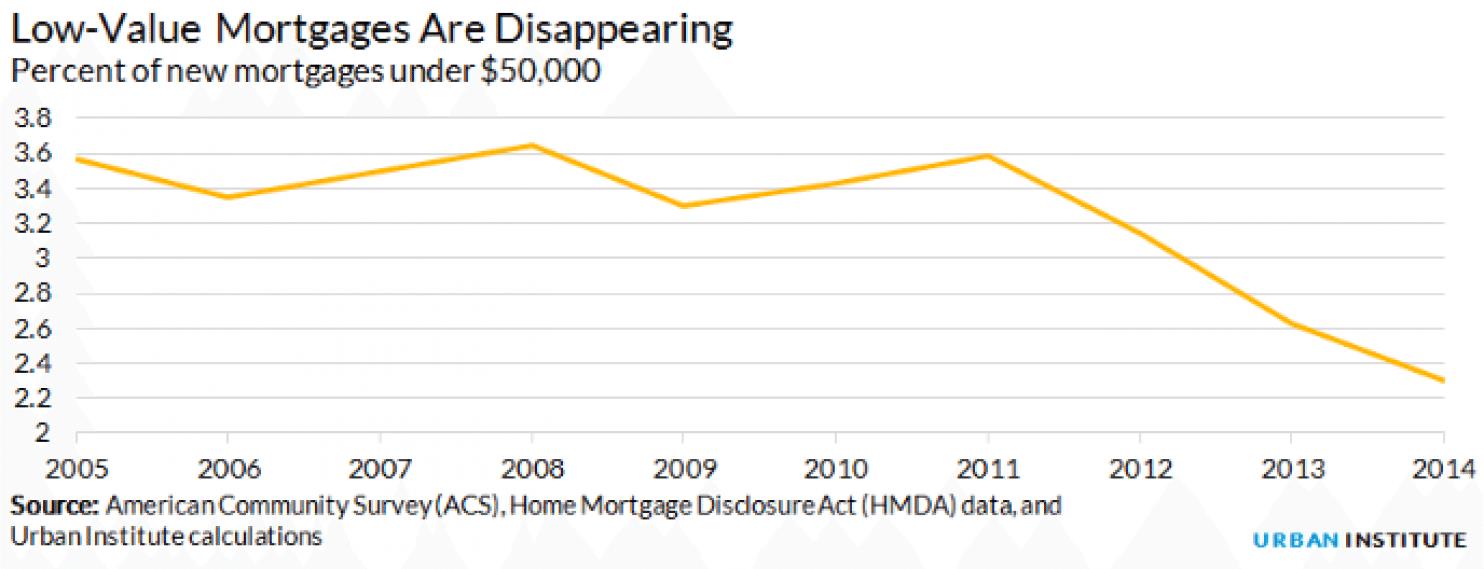

And this has happened as the number of small loans has dwindled:

Urban Institute

So an investor who has bought up thousands of distressed foreclosures for $10,000-$20,000 a piece has to get creative. These properties need expensive repairs, meaning there likely isn’t much profit in repairing and renting them. They aren’t likely to appreciate much over time in stagnant markets like Detroit or Akron, so an investor can’t simply sit on them waiting for a recovery. And these homes can’t easily be sold at a profit to buyers — even with some modest flipping — because buyers in this market can’t get mortgages.

Contract lending, in other words, is just about the most profitable thing an investor could do with these homes. And that opportunity is colliding right now with a time of desperation for would-be buyers.

One way to look at this situation — today or in the 1950s — is that a market failure exists. Something is not working right in the world of legitimate home lending that’s causing families to reach for dubious alternatives, and that’s prompting dangerous models to proliferate. Satter, though, doesn’t see it this way.

“It’s a market success,” she says, viewed from the standpoint of the investors. “They figured out a great way to make a huge amount of money in this situation.”

As for market failures, she says, maybe we should rethink the term. “If you’re looking at how a market works, this is how it works – people saw an opportunity, they came in and grabbed it,” she says. “The market doesn’t care about fair housing for people, or that families need a place to live.”

And that is the other lesson of history that is repeating itself.

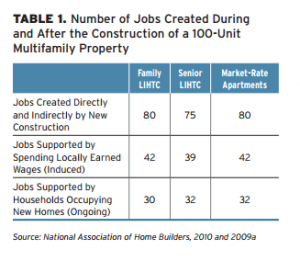

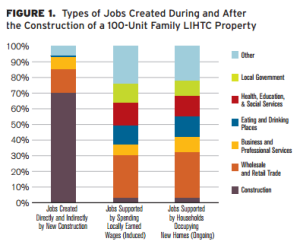

The insufficient supply of housing at a range of affordable prices, especially for rental housing, has important negative impacts on local economic development. Housing costs and availability impacts adequate workforce availability. The causes of high housing costs are multiple but a few factors are controllable by local municipalities, counties and regions with the understanding and political will. Exclusionary housing development zoning regulations for example fall into that category. Housing supply constraints affect local employment opportunities and wage dynamics especially in areas where the degree of zoning regulation barriers are more severe.

It’s getting much tougher to find good jobs in areas with adequate affordable housing opportunities. Even when job markets improve, the absence of strong sustained real income growth means that for more and more communities, the relative cost of housing will continue to climb at the same time the availability of adequately affordable housing is decreasing.

The excellent study referenced above provides a clear discussion of this issue. The primary thesis of the study is that developing more affordable housing in communities creates jobs — both during construction and through new consumer spending after the homes have been occupied. The positive impacts of building affordable rental housing are on par with and in many respects exceed the impacts of developing comparable market-rate units.

The take away from this is that housing affordability, inclusive communities and vibrant economic development, are intertwined in substantial ways. Communities can positively change the dynamics with various policies including favoring appropriate density in zoning laws.

This is the last grant-funded post, so we’ll try to keep it snappy, not sappy. What do we know about housing, anyway? Not a lot, but a good deal more than when we signed on to this gig 10 months ago.

For what they’re worth, we’ll leave you with a gratuitous thought and an anti-climactic ranking.

Housing can’t simply be left to the private market, any more than health care or education. It’s time for people to accept that resolving the housing-affordability crisis will require significant new governmental investment; and alleviating the socioeconomic and racial segregation that continue to stand in the way of fair housing choice, all across the country, will require concerted government intervention. Why shouldn’t the right to decent housing and fair housing choice be a public policy priority commensurate with the right to health care or the right to receive an education?

Rankings abound at New Year, so here’s one with an ancillary question: Rent or buy? 504 counties around the country are listed in order of rental affordability — that is, the percentage of local median income that’s required to pay median rent of three-bedroom apartment in that county. Also listed is the affordability percentage of a median priced home. Compare the percentages to see whether it’s more affordable to rent or buy.

No. 1 in rental affordability (or unaffordability) is Honolulu, at 73 percent. Buy. No. 505 is Huntsville, Ala., at 23 percent. Buy.

The only Vermont county in the table is Chittenden (listed as Burlington/South Burlington). Sorry, Bellows Falls, Bennington, et al, but that’s the way of these national surveys.

Burlington/South Burlington comes in at No. 152 in rental affordability, at 40 percent. Buying affordability: 46 percent. The recommendation: Rent.

That’s despite the fact that, according to the table, the cost of a 3 BR apartment in Burlington/South Burlington went up 12.2 percent in the last year.

Sounds a little high to us (so much for the 3.3 percent figure we’ve been hearing) but again, what do we know?

A key goal of affirmatively furthering fair housing (AFFH), as it’s envisioned playing out around the country, is to break up concentrations of poverty and to promote socioeconomic and racial integration. That means ensuring opportunities for lower-income people and racial minorities to live in wealthier, “high opportunity” neighborhoods with access to jobs, goods schools and public services.

Two ways to facilitate those opportunities:

Promote regional mobility among people with Section 8 vouchers, enabling them to leave high-poverty areas and move into more well-to-do communities. This can require increasing their housing allowance so that they can afford higher suburban rents.

Build affordable, multifamily rental housing in those same, heretofor exclusive neighborhoods.

Both of these approaches deserve consideration around here, as Vermonters contemplate how to make their communities more socioeconomically inclusive. Meanwhile, it’s interesting to see how they’ve played out in an entirely different environment: metropolitan Baltimore.

First, some background: Baltimore has a long history of racial segregation (click here for a trenchant account), and in the mid-1990s, the Department of Housing and Urban Development was sued by city residents (Thompson vs. HUD) for its failure to eliminate segregation in public housing. In 2005, a federal judge found that HUD had violated the Fair Housing Act by maintaining existing patterns of impoverishment and segregation in the city and by failing to achieve “significant desegregation” in the Baltimore region.

Seven years later, a court-approved settlement resolved the case in a way that anticipated the AFFH rule that HUD issued this past summer.

The settlement called on HUD to continue the Baltimore Mobility Program, begun in 2003 in an earlier settlement phase. The program has provided housing vouchers to more than 2,600 families to move out of poor, segregated neighborhoods and into areas with populations that are less than 10 percent impoverished and less than 30 percent black. The program provides counseling before and after the move and has received high marks from evaluators who cite improved educational and employment outcomes for beneficiaries. A similar regional program is underway in Chicago.

The settlement also called for affordable-housing development in these “high-opportunity” suburban communities – 300 units a year through 2020. To make this happen, HUD was to provide new financial incentives for developers.

Here is where the story takes a dispiriting turn. Three years later, not a single developer has applied for the incentives. No affordable housing projects are even in the pipeline. That’s according to an eye-opening story the other day in the Baltimore Sun.

So, what happened? Why haven’t developers shown any interest? HUD had no explanation, according to the story, which suggested that perhaps the program hadn’t been well-enough publicized: a prominent builder of affordable housing admitted he didn’t even know about the incentives. Could it be that they weren’t generous enough?

Whatever the reason, the Baltimore experience reflects how difficult it can be to introduce affordable housing to privileged enclaves. No one should underestimate the AFFH challenge.

for affirmatively furthering fair housing – good work by the New Jersey Housing and Mortgage Finance Agency (NJHMFA)

for affirmatively furthering fair housing – good work by the New Jersey Housing and Mortgage Finance Agency (NJHMFA)