Tag Archives: home ownership

Tampering with the sacrosanct

The presidential candidates have a lot to say about tax reform, but with one exception, they’re not about to get rid the big sacred cow — the mortgage-interest deduction, found on Schedule A of Form 1040:![]()

Economists have been complaining about the mortgage-interest deduction for years. It’s a regressive benefit, increasing with income. It enhances inequality, effectively inflates property values and misallocates resources, or so the argument goes. In 2012, the mortgage interest deduction cost the federal government $70 billion, according to the Urban Institute, compared $36 billion for low-income housing subsidies.

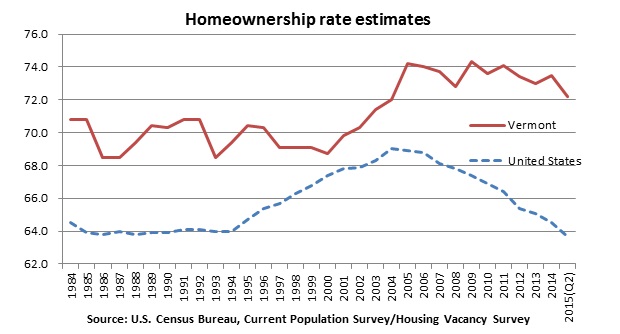

But nobody expects that deduction to go away any time soon. It’s a firmly entrenched loophole (aka “third rail”) not only for the wealthy elite, but for the simple majority. The home ownership rate in this country exceeds 60 percent (in Vermont, it’s over 70 percent), and of course the lion’s share of those people are mortgage-holder beneficiaries.

The ranks of renters are increasing, though, and the more they do, the more seriously they might be taken as a political constituency. Politicians take renters seriously in Germany, where renters are in the majority and the regulatory climate is much more in their favor. Germany doesn’t offer a mortgage-interest deduction, either.

Might the growing numbers of American renters be mobilized to support the elimination of the mortgage-interest deduction — which ostensibly doesn’t benefit them anyway — in favor of increased housing subsidies for low- and moderate-income tenants? That seems like a stretch, unless another Occupy-style movement sweeps the country.

Well, if eliminating the mortgage-interest deduction discourages home ownership, so be it. There’s even evidence that home ownership isn’t necessarily such a wonderful thing, because it damages labor markets:

“We find that rises in the home- ownership rate in a U.S. state are a precursor to eventual sharp rises in unemployment in that state,” write economists David Blanchflower and Andrew Oswald, in a 2013 paper. Why? Partly because higher rates of homeownership curtail labor mobility and lead to longer commutes.

So, who’s the exception among the presidential candidates? Ben Carson.  He’s the only one who has said he’d do away with the mortgage-interest deduction. (Even Bernie Sanders doesn’t go that far – he’d cap it at $300,000.) For a full-throated defense of this Carson stance from someone who doesn’t agree with much of anything else he says, click here.

He’s the only one who has said he’d do away with the mortgage-interest deduction. (Even Bernie Sanders doesn’t go that far – he’d cap it at $300,000.) For a full-throated defense of this Carson stance from someone who doesn’t agree with much of anything else he says, click here.

New population bulge: renters

Renters — and the cost burdens associated with renting — are on the rise across the country. Two recent studies say so, so we might as well cite them here. One, by Enterprise Community Partners and Harvard’s Joint Center for Housing Studies, projects that renter households will increase by 4.2 million over the next 10 years. Another, by the Urban Institute, puts that number at 6 million. And the share of rental households that’s “severely cost-burdened” – that is, paying 50 percent of income or more for housing – will go up 11 to 25 percent under various economic scenarios, says the former study.

Meanwhile, says the Urban Institute, the home ownership rate will go down for all but the oldest population segment. The explanations of these and other stark housing projects are familiar – among them, that college-debt-burdened Millennials aren’t moving into the house-buying market the way their age group did a generation or two ago.

Here we inject the good news/bad news for Vermont.

The home ownership rate here is above the national average and has not mirrored the national drop over the last few years.

Rental cost-burden rates here are, however, about at the national average: 26 percent of Vermont’s renters are “severely cost burdened,” according to Vermont Housing Data.

If the renter population swells in Vermont, how likely is it that the number of affordable housing units keeps pace? Not very, without some form of government intervention. Here’s what the Enterprise/Harvard study says about that:

“The need for affordable housing is already overwhelming the capacity of federal, state and local governments to supply assistance. At last measure, 11.2 million extremely low-income households competed for 7.3 million units affordable to them – a 3.9 million unit shortfall. And with 7.7 million unassisted very low-income renters with worst case housing needs in 2013 as defined by U.S. Department of Housing and Urban Development (HUD), only just over a quarter (26 percent) of eligible very low-income households received rental assistance.”

Now, some might argue that if private developers are simply turned loose to produce a flood of new housing, affordability will take care of itself.

That’s not likely, either. Check out the state of affairs in Portland, Ore., a place that has experienced both a building boom and an unaffordability boom, and where the mayor just declared a “state of emergency for housing and homelessness.”