VSARN (Vermont Student Anti-Racism Network) launched its Racial Equity Report at a virtual press conference on Monday, Aug. 29. VSARN is a Vermont-wide coalition of high school and college students working to combat racial inequities in the state.

The cover of the Racial Equity Report, authored by VSARN

The report includes recommendations to improve racial inequities in Vermont, including revising state curricula for schools to be culturally inclusive, anti-racist, and multicultural and prioritizing restorative justice practices in schools.

Monday’s event opened with comments from the report’s authors, Emily Maikoo, Addie Lentzner, and Minelle Sarfo Adu, and illustrator, Isabella Ingegneri – all of whom are Vermont high schoolers or new college students. Also present were Saudia LaMont, a candidate for the Vermont House, and Rep. Michelle Bos-Lun (D-Westminster) who congratulated the authors on their work, commenting that they were working to fill an educational gap in Vermont schools. Rep. Bos-Lun noted that the report includes recommendations that she hopes to incorporate into future legislative efforts in the Vermont House, in particular restorative justice in schools. The event concluded with questions from the audience.

Minelle Sarfo Adu of South Burlington, a freshman at Antioch University and past CVOEO/Thriving Communities intern, spoke about racial discrimination in housing – noting that BIPOC families are much less likely to be homeowners in Vermont and are disproportionately impacted by rapidly rising rents.

Two of the report’s authors, Addie Lentzner and Emily Maikoo, with report illustrator Isabella Ingegneri, Rep. Michelle Bos-Lun, and Vermont House candidate Saudia LaMont, who all spoke at the launch.

Report highlights

In addition to the recommendations to improve racial inequities in Vermont through changes to policing, criminal legal reform, youth justice efforts, educational curriculum, economic justice, housing equity and supports, healthcare reform, and broad trauma-informed education and anti-bias training, the report includes:

A brief history of racism and slavery in Vermont and its impact on housing discrimination, healthcare, and criminal justice.

The results of the authors’ survey of students at Mount Anthony Union High School, in Bennington, Vt. Key findings included:

79% of respondents said they dis not get a substantial education on race and racism in elementary school

42% of respondents had experienced microaggressions in interactions with teachers

50% of respondents said that is is hard to live in Vermont because of its lack of diversity

Note: All the content below in this post is taken from a web site maintained by the U.S. Department of Housing and Urban Development.

In April, we come together as a community and a nation to celebrate the anniversary of the passing of the Fair Housing Act and recommit to that goal which inspired us in the aftermath of Rev. Dr. Martin Luther King Jr’s assassination in 1968: to eliminate housing discrimination and create equal opportunity in every community.

Fundamentally, fair housing means that every person can live free. This means that our communities are open and welcoming, free from housing discrimination and hostility. But this also means that each one of us, regardless of race, color, religion, national origin, sex, familial status, and disability, has access to neighborhoods of opportunity, where our children can attend quality schools, our environment allows us to be healthy, and [for us to grow] opportunities and self-sufficiency.

…commitment to fair housing is a living commitment, one that reflects the needs of America today and prepares us for a future of true integration.

History of Fair Housing –

On April 11, 1968, President Lyndon Johnson signed the Civil Rights Act of 1968, which was meant as a follow-up to the Civil Rights Act of 1964. The 1968 act expanded on previous acts and prohibited discrimination concerning the sale, rental, and financing of housing based on race, religion, national origin, sex, (and as amended) handicap and family status. Title VIII of the Act is also known as the Fair Housing Act (of 1968).

The enactment of the federal Fair Housing Act on April 11, 1968 came only after a long and difficult journey. From 1966-1967, Congress regularly considered the fair housing bill, but failed to garner a strong enough majority for its passage. However, when the Rev. Dr. Martin Luther King, Jr. was assassinated on April 4, 1968, President Lyndon Johnson utilized this national tragedy to urge for the bill’s speedy Congressional approval. Since the 1966 open housing marches in Chicago, Dr. King’s name had been closely associated with the fair housing legislation. President Johnson viewed the Act as a fitting memorial to the man’s life work, and wished to have the Act passed prior to Dr. King’s funeral in Atlanta.

Another significant issue during this time period was the growing casualty list from Vietnam. The deaths in Vietnam fell heaviest upon young, poor African-American and Hispanic infantrymen. However, on the home front, these men’s families could not purchase or rent homes in certain residential developments on account of their race or national origin. Specialized organizations like the NAACP, the GI Forum and the National Committee Against Discrimination In Housing lobbied hard for the Senate to pass the Fair Housing Act and remedy this inequity. Senators Edward Brooke and Edward Kennedy of Massachusetts argued deeply for the passage of this legislation. In particular, Senator Brooke, the first African-American ever to be elected to the Senate by popular vote, spoke personally of his return from World War II and inability to provide a home of his choice for his new family because of his race.

With the cities rioting after Dr. King’s assassination, and destruction mounting in every part of the United States, the words of President Johnson and Congressional leaders rang the Bell of Reason for the House of Representatives, who subsequently passed the Fair Housing Act. Without debate, the Senate followed the House in its passage of the Act, which President Johnson then signed into law.

The power to appoint the first officials administering the Act fell upon President Johnson’s successor, Richard Nixon. President Nixon tapped then Governor of Michigan, George Romney, for the post of Secretary of Housing and Urban Development. While serving as Governor, Secretary Romney had successfully campaigned for ratification of a state constitutional provision that prohibited discrimination in housing. President Nixon also appointed Samuel Simmons as the first Assistant Secretary for Equal Housing Opportunity.

When April 1969 arrived, HUD could not wait to celebrate the Act’s 1st Anniversary. Within that inaugural year, HUD completed the Title VIII Field Operations Handbook, and instituted a formalized complaint process. In truly festive fashion, HUD hosted a gala event in the Grand Ballroom of New York’s Plaza Hotel. From across the nation, advocates and politicians shared in this marvelous evening, including one of the organizations that started it all — the National Committee Against Discrimination In Housing.

In subsequent years, the tradition of celebrating Fair Housing Month grew larger and larger. Governors began to issue proclamations that designated April as “Fair Housing Month,” and schools across the country sponsored poster and essay contests that focused upon fair housing issues. Regional winners from these contests often enjoyed trips to Washington, DC for events with HUD and their Congressional representatives.

Under former Secretaries James T. Lynn and Carla Hills, with the cooperation of the National Association of Homebuilders, National Association of Realtors, and the American Advertising Council these groups adopted fair housing as their theme and provided “free” billboard space throughout the nation. These large 20-foot by 14-foot billboards placed the fair housing message in neighborhoods, industrial centers, agrarian regions and urban cores. Every region also had its own celebrations, meetings, dinners, contests and radio-television shows that featured HUD, state and private fair housing experts and officials. These celebrations continue the spirit behind the original passage of the Act, and are remembered fondly by those who were there from the beginning.

On Nov, 8, voters across the country heard the affordable housing call and approved numerous state and local housing funding measures that will make it possible for more of our neighbors to live in safe, healthy, and affordable homes. This was a real achievement in housing advocacy, but the work is far from over. Developers, local governments, and advocates must now move to convince the neighbors of proposed housing developments to accept more affordable homes into their communities.

The election that brought over 37 affordable housing measures to the ballot in eight states also elevated toxic rhetoric about people of color and other populations. The public discourse has changed, and that’s likely to affect our efforts to build support for affordable housing development and counter community opposition. Here’s what you may hear about affordable housing in your community, and how to prepare for it:

Racial animus. In the wake of the election, there have been many reports of hate-based harassment and intimidation across the country. An offending segment of our population feels newly empowered to use racist language in all types of situations. While racism and fear of difference have always been, at the very least, an undercurrent of some forms of community opposition, in recent years it’s largely been implied, not overt. You may see an uptick in overt racism in siting conversations.

What to do? While it would be satisfying—and, arguably, right—to call out racist language directly when you hear it, research tells us that this is likely to backfire, causing the speaker to defensively double-down on the prejudiced belief. Instead, a study this year found that “a short conversation encouraging actively taking the perspective of others can markedly reduce prejudice.” It argues for holding small-group conversations and facilitators trained to listen and find common ground.

Misinformation. You’ve likely heard much about the success of fake news during the presidential campaign. Misinformation this election cycle may have had a distinctive rightward bent, but don’t pat yourself on the back if you lean left. All of us are susceptible to information that confirms what we already believe, regardless of its factual accuracy. Don’t be surprised to see an increase in the misinformation about your work being posted online and handed around in anonymous flyers around the neighborhoods where you work.

What to do? Don’t write up a “frequently asked questions” page correcting the lies being told about your work. By emphasizing the misinformation—even when you later correct it—you’re just driving it deeper into peoples’ consciousness. Instead, first tell your truth (“Our apartments increase neighborhood safety.”), then signpost the misinformation and explain the motive behind it (“There is a myth circulating that affordable housing increases crime, promoted by a small new neighborhood group formed to fight our proposal.”), and finally give a brief, clear alternative explanation, repeated in graphics if possible (“In fact, by starting a neighborhood watch program and installing security cameras, we’ve helped create a 13 percent decrease in property crime in another neighborhood where we work. We want to work with you to have a similar positive impact here.”).

Ideological conflict.Research into persistent opposition to affordable housing has shown that spatial ideology—an individual’s set of beliefs around who can live in and use a particular place, and who has the right to participate in decision-making about a place—can be predictive of opposition to, or support of, affordable housing. The recent push to disenfranchise groups of Americans through voter ID laws and other restrictions is an example of a narrow conception of spatial rights, and the electoral contest was rife with rhetoric supporting a conscribed idea of to whom America truly belongs. Opposition may now more frequently focus on delegitimizing prospective low-income residents, perhaps as “not American” or simply “not from here.”

What to do?Unfortunately, ideology might be hard-wired, and thus addressing spatial ideology head-on might not be effective. At the same time, there are likely to be people in your community who believe lower-income people have an equal right to live in a place. Find these potential supporters by emphasizing the values of diversity and inclusion, and give this group a clear way to take action and vocalize support of your work.

Distrust of institutional authority. The success of populist presidential candidates from both parties points to, among other things, Americans’ growing distrust of institutions. Whether it’s in banks, the news media, or government itself, people across the political spectrum have lost faith. Unfortunately, affordable housing development connects to all sorts of things many of our neighbors have come to doubt: taxation, finance systems and entities, and zoning, just to name a few.

What to do? First, people who have lost trust will hear a developer mention “partnering with the government” and translate that into an attempt to paper over a profit-making arrangement. Step away from the marketing talk and use plain language to explain what you do, and why it is successful. Second, reframe the role of these perceived-suspect institutions. A new paper from Enterprise Community Partners and the FrameWorks Institute recommends that we help people understand the role of government in affordable housing by explaining, “the role of systems in shaping outcomes for people and … communities,” and by, “zooming out” to tell broader stories that explain the impact of housing issues on an entire community. You know your work is about more than simply units; help others understand this too.

Countering community opposition has never been easy, and I hope to hear that these predictions have not come true, but even if they do, our work can have a long-term impact on decreasing bias. There is evidence that white people living in diverse neighborhoods “endorsed fewer negative stereotypes, and [feel] closer to Blacks as a group.” When we create diverse, inclusive communities, we help decrease prejudice and division. That’s something truly worth fighting for.

Beryl Satter knew something like this was bound to happen. Or, rather, to happen again.

The Rutgers historian wrote the book on an obscure form of predatory lending from the mid-20th century that victimized black home buyers when banks would not lend them mortgages. Her book, “Family Properties,” came out in 2009, on the heels of the housing crash. And as she traveled the country talking about it — about families defrauded from the homes they thought they owned, about sellers who promised home ownership but collected deposits and evictions instead — people kept approaching her.

“Pretty much everywhere I go, people say ‘I’ve been hearing about this,'” Satter says. “Contract” lending is making a comeback.

In this model, buyers shut out from conventional lending are offered an alternative: They can make monthly payments on a home directly to the seller, instead of a bank, with the promise of receiving the deed only once the property is entirely paid off, 20 or 30 years down the road. In the meantime, they have few of the legal protections of a typical home buyer but all of the responsibilities of one. They don’t build equity with time. They can be easily evicted. And if that happens, they lose all of their investment.

According to the Detroit Free Press, more homes were bought in Detroit last year using such “land contracts” or “contracts for deeds” than conventional mortgages. In a series of recent stories, the New York Times has reported that Wall Street is now betting on this market, with investors buying foreclosed homes by the thousands and selling them on contract. Earlier this week, the Times reported that the Consumer Financial Protection Bureau is now investigating the practice’s resurgence, although it is not by definition illegal.

What is particularly alarming about the trend, though, is that we’ve seen it before. In its earlier incarnation, it was an explicitly racist form of exploitation. And now it is victimizing the same groups again: mostly lower income and minority home buyers who can’t access traditional credit.

“There’s nothing new here in the slightest,” Satter says. “This is just a continuation of the same old game. That’s what’s so disturbing.”

In the earlier era when this was common, between the 1930s and 1960s, contract lending was in some cities the primary means middle-class blacks had to buy homes. Real estate agents and speculators jacked up the price of properties two- or threefold. Then when families fell behind on a month’s payment or on repairs, they were swiftly evicted. The sellers kept their deposits and found the next family.

Satter’s father, Chicago lawyer Mark Satter, helped organize black Chicagoans to fight the practice in the 1950s. He estimated then that about 85 percent of homes bought by black in Chicago were bought on contract. “It was the way you bought,” Beryl Satter says. “There was no other way.”Many of those families then struggled to keep their homes in a system that was not sustainable by design.

Atlanticwriter Ta-Nehisi Coates based his blockbuster 2014 article “The Case for Reparations”around the story of Chicago blacks who suffered under this system, the outgrowth, as he put it, of a segregated city with “two housing markets — one legitimate and backed by the government, the other lawless and patrolled by predators.”

The Times reports of what’s happening today sound eerily similar. Writers Matthew Goldstein and Alexandra Stevenson report that an estimated 3 million people have bought homes through contracts, although the numbers are hard to track given that the deals are regulated differently in each state and are not subject to the same disclosures as mortgages.

The practice is particularly common, they report, in distressed Midwestern communities like Akron and Detroit, where the government offered hundreds of foreclosed properties to investors in bulk sales. Those same investors, the Times reports, have turned around and sold the properties on contract to moderate-income buyers for sometimes four times as much.

Why now?

But why, though, would a financial scheme created in an era of sanctioned racial discrimination be making a resurgence today? Since Satter’s father tried to sue over the tactic a half-century ago, the Fair Housing Act and Home Mortgage Disclosure Act were passed. And the end of legal discrimination opened up legitimate lending to more blacks who were no longer forced into the housing market’s rapacious underworld.

But a crucial similarity between the two eras exists: Many people still can’t get loans today.

Now, this is the case because lenders have tightened their credit standards since the crash, overcorrecting for the bubble’s exuberance with historic stinginess. The Urban Institute has counted more than 5 million loans currently “missing” from the housing market — mortgages that would have been made between 2009 and 2014 if lenders used the kind of credit standards that were common back in 2001, a benchmark for more reasonable lending prior to the housing bubble.

Millions of Americans over this same time have had their credit ruined by foreclosures — in many cases because of predatory subprime lending that has now put them in the crosshairs of predatory land contracts. Minorities who were disproportionately targeted for the former are not surprisingly concentrated among those caught up in the latter.

“When the banks close down, people still need to buy,” Satter says. And so they find a way. Just as creative investors find a way to meet their demand. Land contracts are to housing whatpayday loans are to banking and Rent-A-Centers are to furniture. What people in need can’t access through credit someone is always willing to provide — for a price.

A lawyer for Harbour Portfolio Advisors in Dallas, one of the larger players in the new wave of contract lending, told the Times that the firm’s business model is “to purchase unproductive residential properties and sell them to other people who will make them productive again.” But Satter frames this differently.

“Choices that black Americans have had for housing loans have been predatory loans, or no loans,” she says. And when banks choose not to loan, she adds, this is who they choose not to loan to.“The result,” Satter says, “is a complete revival of redlining in a slightly different guise.”

This is why she wasn’t surprised to see the practice she’d studied as a historian (and lived through with her family in the 1950s) re-emerge as front-page news.

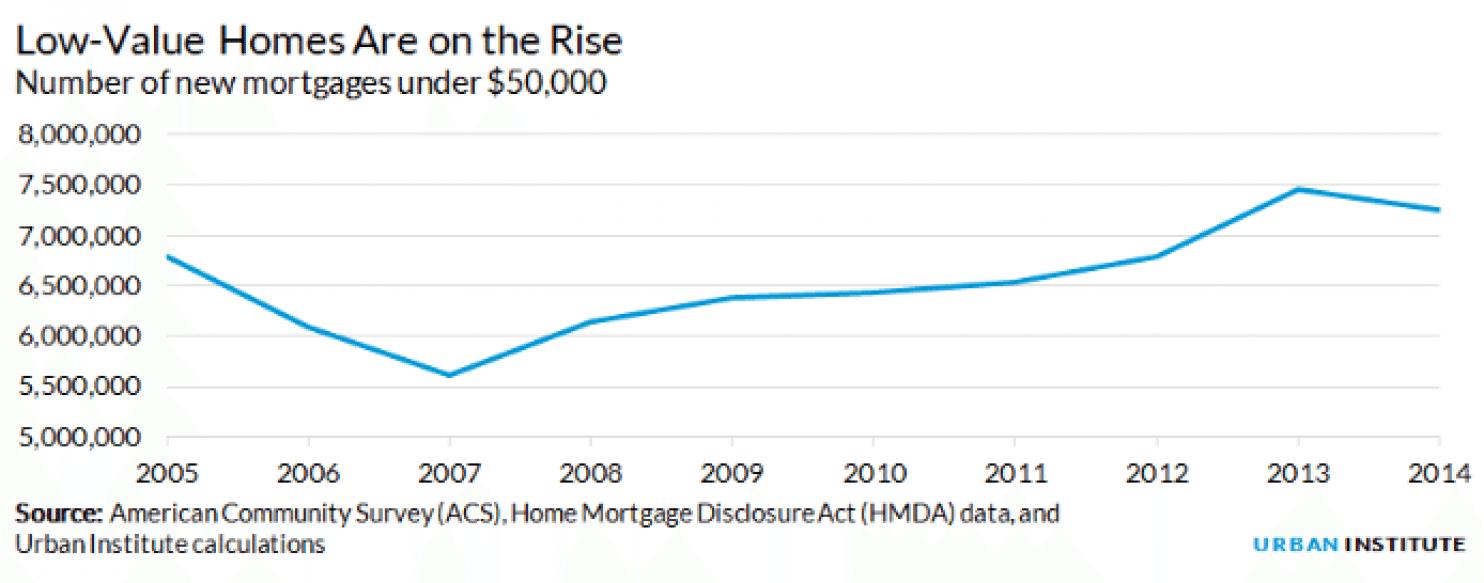

One other factor, though, helps explain why contract selling is back again. The demand among buyers who can’t get mortgages is deep. But so is the supply of houses that might accommodate buyers at the moderate end of the market. The foreclosure crisis created a vast stock of vacant homes, many of which have deteriorated through neglect. Steven Brown, an affiliated scholar at the Urban Institute, has shown that the number of homes worth less than $50,000 has been growing:

Urban Institute

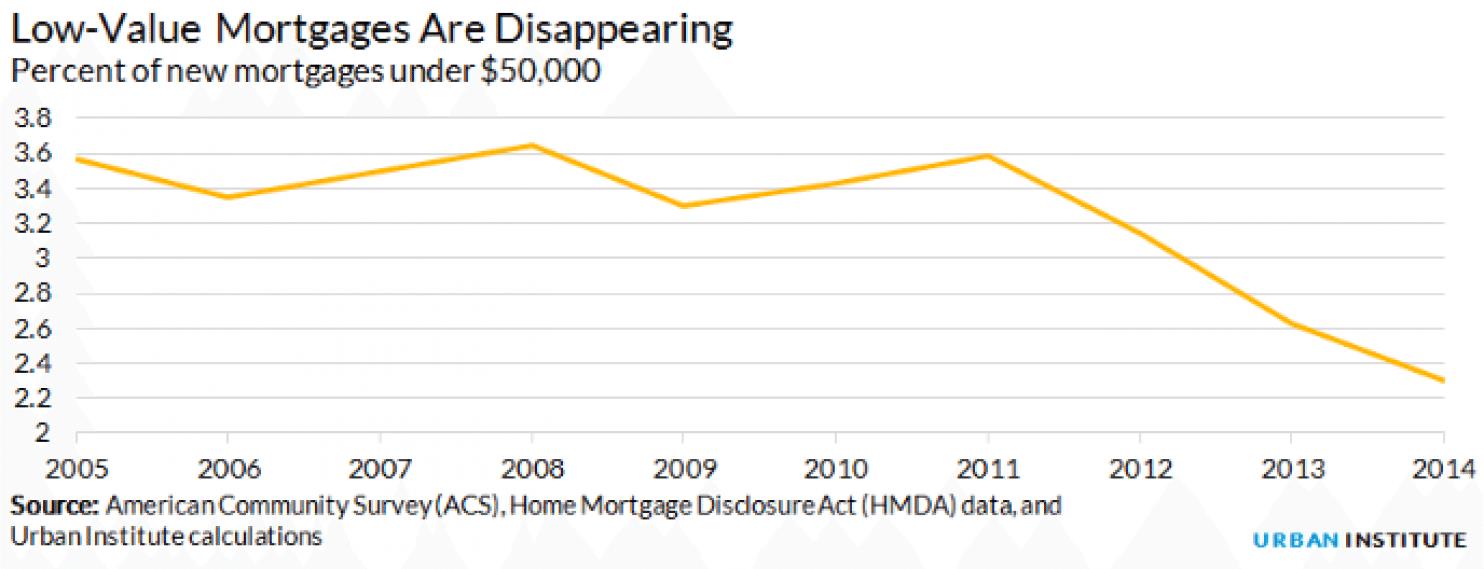

And this has happened as the number of small loans has dwindled:

Urban Institute

So an investor who has bought up thousands of distressed foreclosures for $10,000-$20,000 a piece has to get creative. These properties need expensive repairs, meaning there likely isn’t much profit in repairing and renting them. They aren’t likely to appreciate much over time in stagnant markets like Detroit or Akron, so an investor can’t simply sit on them waiting for a recovery. And these homes can’t easily be sold at a profit to buyers — even with some modest flipping — because buyers in this market can’t get mortgages.

Contract lending, in other words, is just about the most profitable thing an investor could do with these homes. And that opportunity is colliding right now with a time of desperation for would-be buyers.

One way to look at this situation — today or in the 1950s — is that a market failure exists. Something is not working right in the world of legitimate home lending that’s causing families to reach for dubious alternatives, and that’s prompting dangerous models to proliferate. Satter, though, doesn’t see it this way.

“It’s a market success,” she says, viewed from the standpoint of the investors. “They figured out a great way to make a huge amount of money in this situation.”

As for market failures, she says, maybe we should rethink the term. “If you’re looking at how a market works, this is how it works – people saw an opportunity, they came in and grabbed it,” she says. “The market doesn’t care about fair housing for people, or that families need a place to live.”

And that is the other lesson of history that is repeating itself.

This is the last grant-funded post, so we’ll try to keep it snappy, not sappy. What do we know about housing, anyway? Not a lot, but a good deal more than when we signed on to this gig 10 months ago.

For what they’re worth, we’ll leave you with a gratuitous thought and an anti-climactic ranking.

Housing can’t simply be left to the private market, any more than health care or education. It’s time for people to accept that resolving the housing-affordability crisis will require significant new governmental investment; and alleviating the socioeconomic and racial segregation that continue to stand in the way of fair housing choice, all across the country, will require concerted government intervention. Why shouldn’t the right to decent housing and fair housing choice be a public policy priority commensurate with the right to health care or the right to receive an education?

Rankings abound at New Year, so here’s one with an ancillary question: Rent or buy? 504 counties around the country are listed in order of rental affordability — that is, the percentage of local median income that’s required to pay median rent of three-bedroom apartment in that county. Also listed is the affordability percentage of a median priced home. Compare the percentages to see whether it’s more affordable to rent or buy.

No. 1 in rental affordability (or unaffordability) is Honolulu, at 73 percent. Buy. No. 505 is Huntsville, Ala., at 23 percent. Buy.

The only Vermont county in the table is Chittenden (listed as Burlington/South Burlington). Sorry, Bellows Falls, Bennington, et al, but that’s the way of these national surveys.

Burlington/South Burlington comes in at No. 152 in rental affordability, at 40 percent. Buying affordability: 46 percent. The recommendation: Rent.

That’s despite the fact that, according to the table, the cost of a 3 BR apartment in Burlington/South Burlington went up 12.2 percent in the last year.

Sounds a little high to us (so much for the 3.3 percent figure we’ve been hearing) but again, what do we know?

It seems that the wide-ranging portfolio of Warren Buffett, investment sage and one of the world’s richest men, includes a mobile-home empire that’s coming under fair-housing scrutiny.

That’s Clayton Homes Inc., the leading maker of mobile homes, which Buffett’s Berkshire Hathaway bought in 2003. A Clayton affiliate is also the leading lender to purchasers of mobile homes.

Now comes an investigative series by the Seattle Times, the Center for Public Integrity and BuzzFeed alleging exploitative lending to minorities, not to mention racist employment practices. One of the key predatory-lending allegations is summed up by this sentence, the series’ third article published the other day:

“The company’s in-house lender, Vanderbilt Mortgage, charges minority borrowers substantially higher rates, on average than their white counter parts. In fact, federal data shows that Vanderbilt typically charges black people who make over $75,000 a year slightly more than white people who make only $35,000.”

To this and the series’ accusations launched beginning in April, Clayton issued a “categorical” denial in a press release dated Dec. 26, stating, among other things:

“(I)n 2015, for borrowers with credit scores less than 600 who chose to purchase a home-only placed on private land, and borrowed less than $50,000, the average note rate from Vanderbilt was the same for white and non-white borrowers. For borrowers with credit scores greater than 720, the note rate for non-white borrowers was 0.07 percent less than for white borrowers.”

Buffett stands by the company and told shareholders this past spring that he “makes no apologies whatsoever for Clayton’s lending terms.”

Most of the alleged depredations highlighted in the articles have taken place in the south and on native American reservations in the Southwest. Clayton does have a presence in Vermont. The company’s website lists two sales outlets in the state – in Montpelier and White River Junction – out of more than a thousand dealerships nationwide.

If the series’ allegations have legs, one might expect they’ll prompt a federal investigation or a reverse-redlining lawsuit of the sort that was lodged against Wells Fargo for preying on minority home-buyers in Baltimore and Memphis in the years leading up to the housing bust.

Little backyard houses — aka “accessory dwelling units” — are springing up all over Vancouver. This is a partial remedy to the affordable rental shortage that afflicts municipalities all over North America, including Vermont. It also affords an optional living arrangement for older people who want to age in place. In Vancouver, these appendages are called “laneway houses,” and some of them are pretty handsome. There’s plenty of room for additions like this in Burlington, even if we don’t have alleys — and in plenty of other Vermont communities, too.

A “mobility program” in heavily segregated Baltimore moves families from high-poverty public housing complexes in the city to higher-rent, higher-opportunity suburbs. This is an initiative very much in the spirit of affirmatively furthering fair housing, but it serves a small fraction of the subsidy-eligible families in need and it operates largely under the radar, to minimize opposition. One obstacle: a shortage of affordable housing in suburban communities.

Plattsburgh has a new 64-unit affordable housing complex, called Homestead on Ampersand. It’s just a couple of miles from the neighborhood where complaints about a proposal for a smaller affordable housing complex prevailed.

Columbus, Ohio, plans to transform a vacant downtown building into “workforce housing” – which in this case means housing for people who make $40,000 to $60,000 a year. The made-over building would feature micro units – apartments of 300 square feet or so and targeted, presumably, to single Millennials. We’ve touched on the micro movement before, which seems to be taking hold mostly in bigger metro areas (here’s a roundup with a national map; for a more substantial study of the phenomenon, click here). But it has also spread to Kalamazoo and, as we’ve noted, Syracuse, so there’s no reason it couldn’t work in an over-priced city like Burlington, where officialdom is forever wringing its hands about how young professionals have trouble finding affordable accommodations.